Retailers have spent years and serious budget making personalization smarter, with better recommendations, dynamic journeys, and AI tuned to every signal they can capture. Which raises a simple question that’s rarely asked: what is all of it actually for?

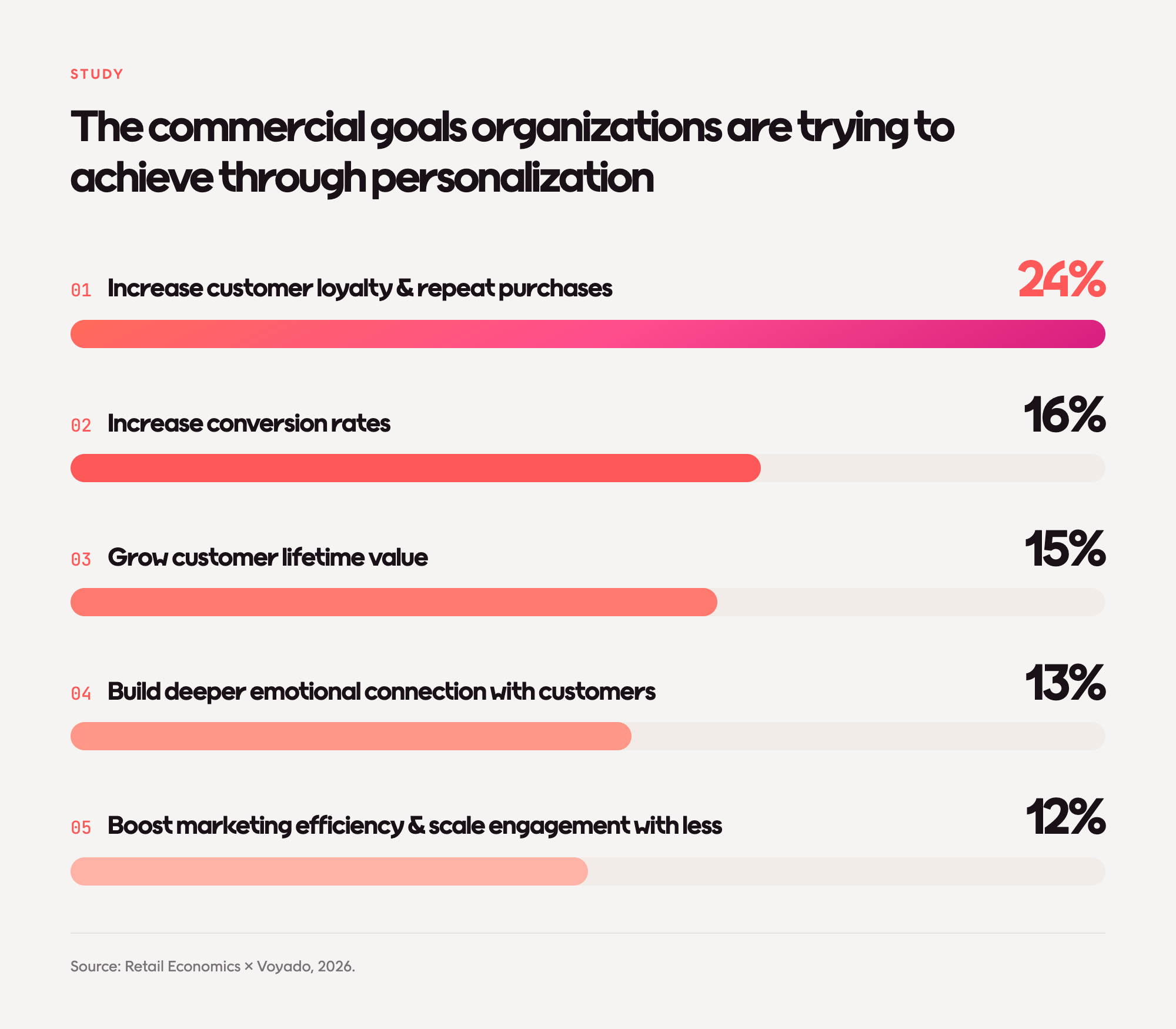

We asked retailers directly, and the answer was unambiguous: Loyalty. It ranks ahead of conversion, lifetime value growth, emotional connection, and efficiency as the top goal for personalization.

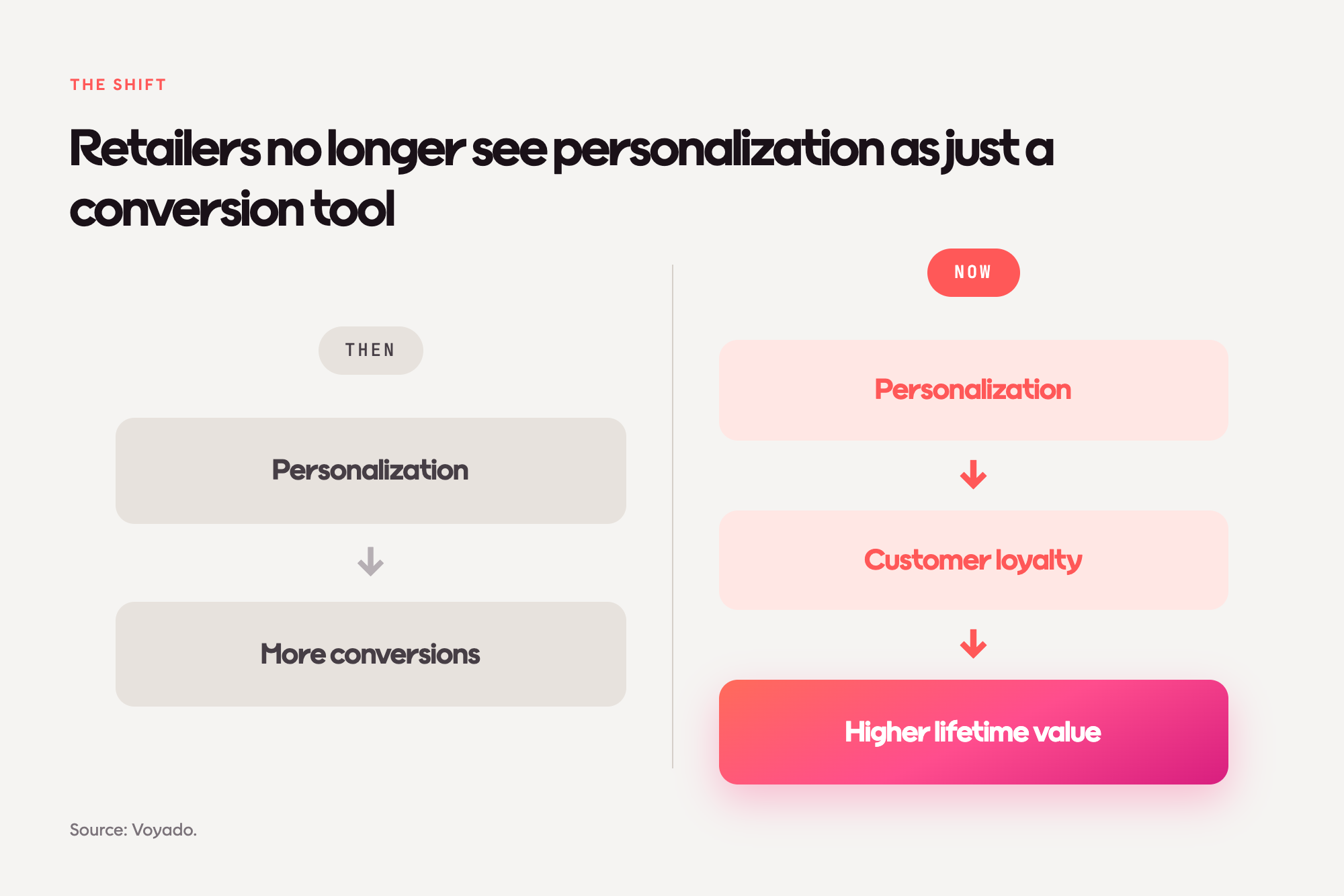

That answer changes how the personalization conversation should be framed. Retailers aren’t reaching for AI to cut headcount or shave a few basis points off conversion, but to build something harder and more valuable: customers who come back, spend more, and stay longer.

The finding: loyalty leads, and retention dominates

The data is unambiguous (and more nuanced than a single headline).

Loyalty ranks first, but read the whole ranking, and something else jumps out. Lifetime value growth appears separately at 15%, third overall. These are two different things: loyalty is the behavior retailers want to build, and CLV growth is the financial measure of that behavior paying off. But they point in the same direction. Combined, they account for nearly 40% of retailers’ primary goals for personalization. This is more than twice the share focused on winning new customers through conversion.

The story the ranking tells, therefore, isn’t “loyalty vs. everything else.” It’s retention vs. acquisition, and retention is winning by a long way.

Why retention, and why now

Retailers aren’t picking loyalty as a soft preference. They’re picking it because the economics of retail have changed.

Ask retailers what’s driving this shift, and the answer that comes back most often is the cost of the alternative. Paid acquisition has become significantly more expensive year on year. First-party data restrictions have made it harder to target new audiences. Consumer switching between brands has increased. In that environment, every bit of budget spent acquiring a customer you already have is budget wasted — and every existing customer who lapses is one you’ll have to pay to replace at rising cost.

That reasoning came up repeatedly in conversations we’ve had with retail teams evaluating their personalization strategy. In one such conversation, a retail leader framed it plainly: acquiring new customers has become expensive, so the goal now is turning the customers they already have into returning ones. That instinct isn’t unique to one market or category. It’s the reasoning behind why 40% of retailers now prioritize keeping customers over winning new ones.

How retailers think personalization drives loyalty

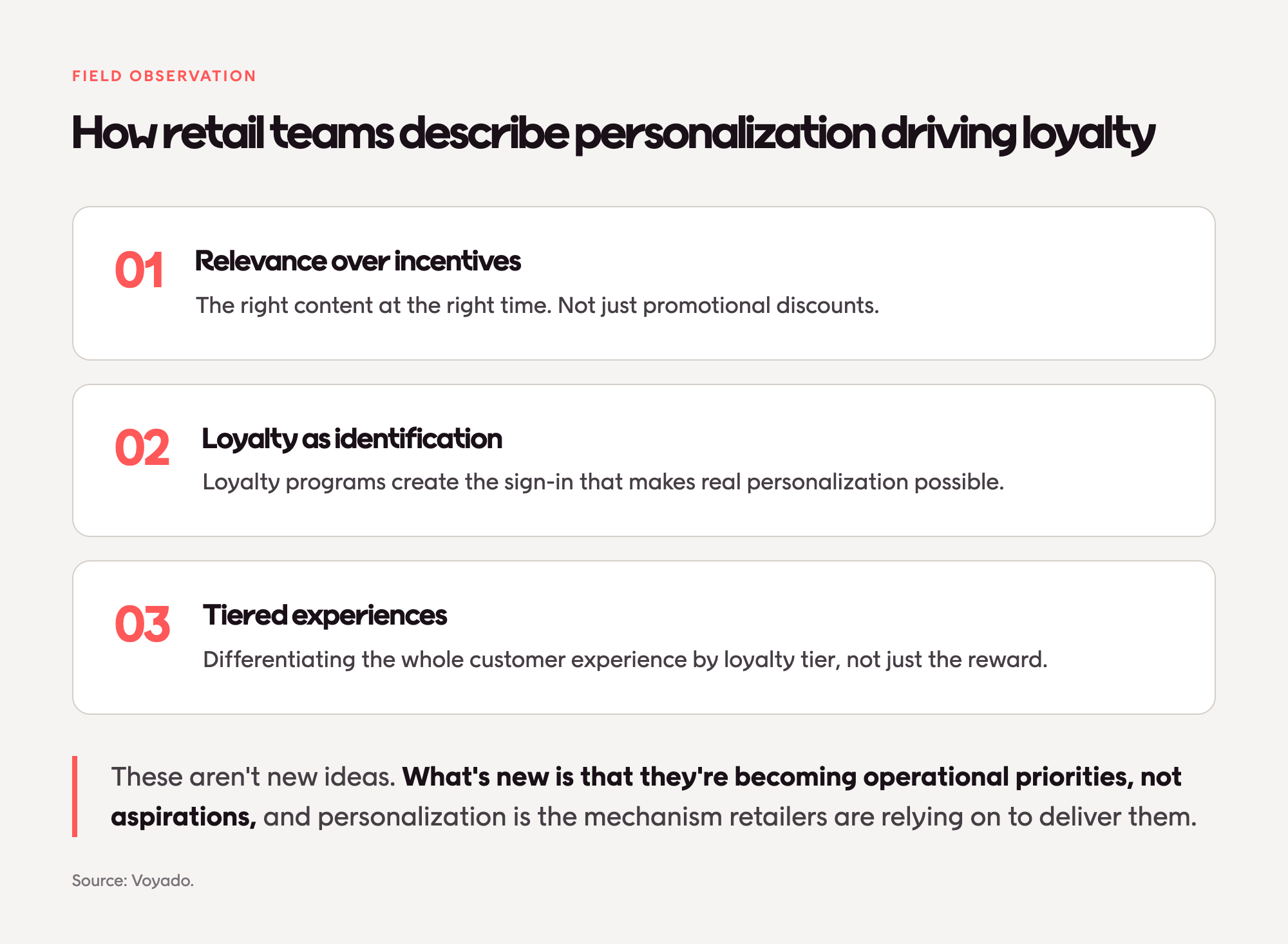

The finding that loyalty leads is one thing. The mechanism retailers are betting on, namely how they think personalization creates loyalty, is another. And the picture that emerges from conversations is more specific than “personalize more,” with three mechanisms coming up repeatedly:

Relevance over incentives

Retail teams increasingly reject the idea that loyalty is built through discounts. What they describe wanting instead is the right content at the right time to the right person, across email, SMS, on-site experience, and in-store, delivered consistently rather than as one-off campaigns. Some might say that discounting is what retailers do when they’re struggling with relevance. It’s a shortcut with a compounding cost, because a customer acquired or reactivated on price is a customer who will likely lapse on price too.

Loyalty as an identification hook

There’s a more practical dynamic underneath this too: personalization and loyalty don’t just share a goal, they depend on each other to work. Loyalty programs give customers a reason to identify themselves; that identification unlocks the data personalization needs to actually work. This flips the usual framing: loyalty isn’t the output of good personalization, but part of the input. Without identified customers, personalization defaults back to broad segmentation and probabilistic guessing.

Tiered experiences, not just tiered rewards

Where mature loyalty strategies used to be about points and discounts at different levels, retail teams now describe wanting to differentiate the experience itself by loyalty tier. Different product showcases, different content, different service moments: all made operationally possible at scale through personalization.

Why the loyalty level varies by category

One thing the ranked data hides is how differently loyalty translates across retail categories. Loyalty leads overall, but zoom in, and the specific goal, and therefore what personalization should be tuned to, shifts significantly.

| Category | Primary personalization goal |

| Mid-market fashion | Lifetime value growth |

| Premium fashion | Customer loyalty & brand equity |

| Electronics | Customer loyalty & repeat purchase |

Among the categories with a large enough sample to report confidently, a strong pattern emerges: fashion and electronics both prioritize retention-flavored goals, but for different reasons. Mid-market fashion needs repeat purchasing to sustain margin, so lifetime value is the operational target. Premium fashion protects brand equity through long-term relationships, so loyalty as brand loyalty is the priority. Electronics operates in a commoditized market where the product itself doesn’t differentiate, so the customer relationship is where competition happens.

Smaller categories in the study, like furniture and health and beauty, hint at further variation, with furniture skewing toward maximizing value at infrequent, high-consideration purchase moments, and health and beauty leaning toward emotional connection between purchases. The pattern is directional rather than quantifiable at our sample sizes, but the underlying point holds: personalization isn’t one strategy applied uniformly. It’s a set of category-specific plays that happen to share loyalty as the common ambition.

Why this matters

The framing shift here matters more than the ranking. Personalization has too often been sold and evaluated as a tool for lifting immediate conversion. The data says retailers themselves are already past that framing. Instead, they’re using personalization to change the shape of their customer base, rather than just to move next week’s numbers.

That has implications for how personalization is planned, measured, and reported within a business. If loyalty is the goal, the metrics that judge personalization can’t be only click-through and conversion. If retention is worth twice acquisition in retailers’ own priorities, the personalization investment should be judged on repeat purchase, value over time, and lapse rates, not just what happened in the campaign window.

The retailers already moving in this direction have made one practical change: they’ve stopped judging personalization on campaign metrics and started judging it on customer ones. Repeat purchase rate. Customer lifetime value. Lapse rate. And that shift in measurement is what pulls personalization strategy toward loyalty, not away from it.

Methodology

This article draws on primary research conducted by Retail Economics, an independent economics research consultancy specializing in the retail and consumer sectors.

Survey of retail decision-makers Retail Economics surveyed 300 marketing and e-commerce leaders across Benelux (Belgium, Netherlands, Luxembourg), DACH (Germany, Austria, Switzerland), Scandinavia (Norway, Sweden, Denmark), and the UK in December 2025. Respondents held senior roles across marketing, e-commerce, CRM, and digital functions. Where findings are broken down by retail category, base sizes vary. Categories with fewer than 30 respondents are noted as directional rather than statistically robust.

About Author