Black Week 2025 arrived with fewer dramatic swings than in previous years, yet the results still offer useful signals about how shoppers engaged throughout the period.

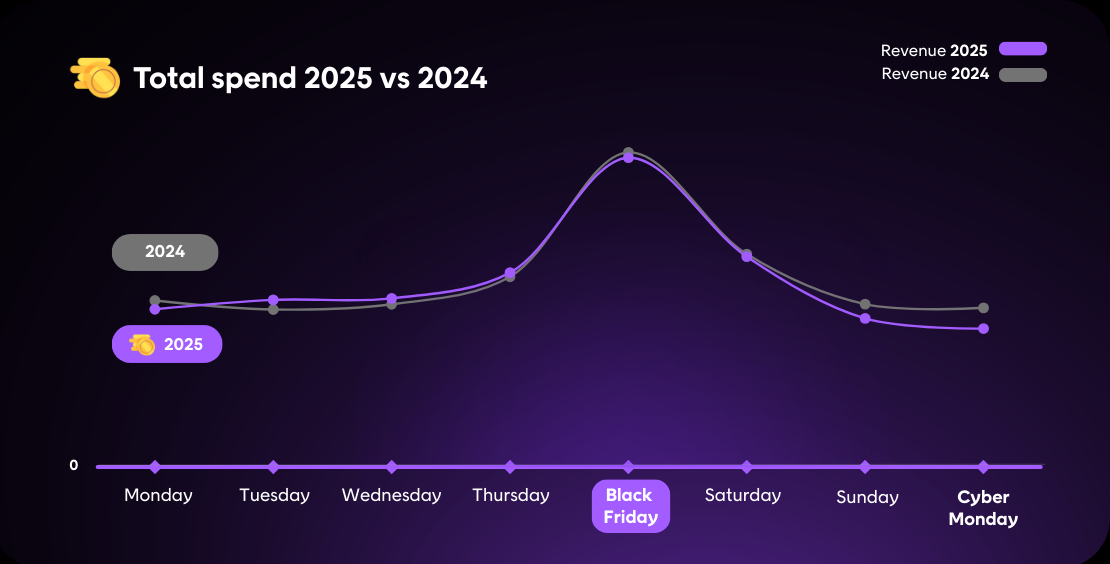

Total consumer spending across the 11 core verticals was just slightly below last year at -1%. While the overall shift is modest, the distribution of that spend – when people purchased, where they shopped, and which categories gained the most traction – provides helpful context for retailers planning for 2026.

To support this, we’ve published a full breakdown of results across all industries on our Black Week benchmarks page, including daily trends and sector-level performance.

In this article, we take a closer look at the patterns within the week: how activity developed across different days, where in-store and online channels diverged, and which sectors showed steady growth versus more cautious movement. We also share how the Voyado platform supported record operational volume through the week and what retailers might take away as they prepare for the year ahead.

For anyone looking to benchmark their own performance or get a clearer picture of how Black Week unfolded, the data offers some valuable insights.

Black Week 2025 overview

|

A stable week on the surface, but not in the details

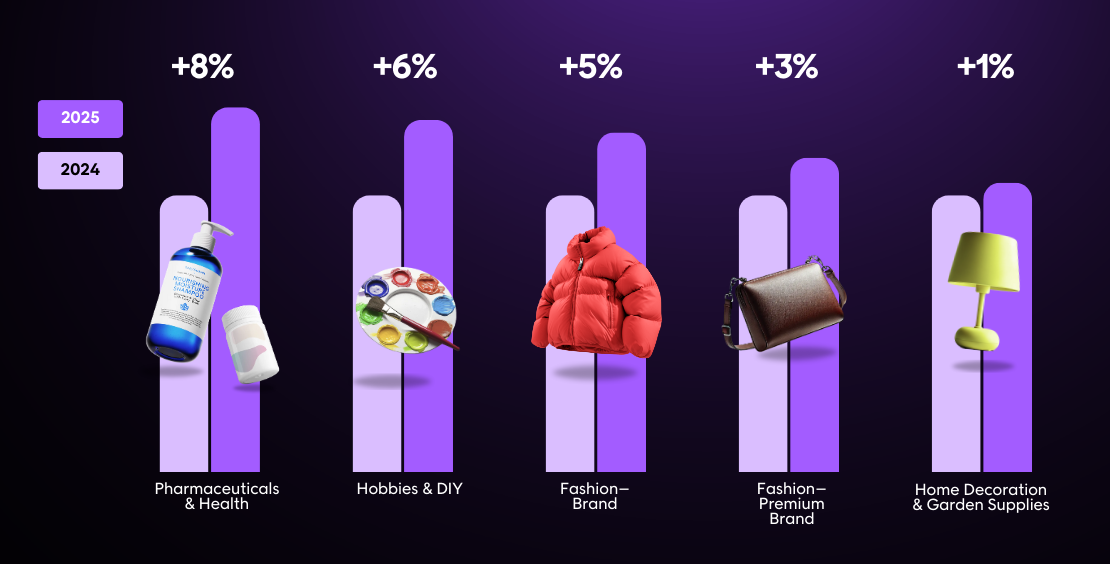

Overall consumer spend showed only a slight decline, but sector-level performance showed bigger differences.

Pharmaceuticals & Health recorded the strongest full-week growth at +8%, followed by Hobbies & DIY at +6%, and Fashion – Brand at +5%. This might suggest that these categories benefited from stable demand: wellness, lifestyle projects, and quality-focused fashion remained priorities for many shoppers.

Other sectors, such as Electronics, Sports & Outdoor, and Jewelry & Accessories, held relatively steady, indicating consistent shopper behavior even in a competitive environment.

The result is a more nuanced picture of Black Week performance: pockets of notable growth, areas of stability, and sectors more sensitive to promotional timing or economic conditions.

Sector performance snapshotFastest-growing sectors:

Steady sectors:

Most pressured sectors:

|

The rise of the early-week shopper

This year, some of the strongest activity took place earlier than expected. For many categories such as Fashion – Brand, Hobbies & DIY, Home Decoration & Garden, and Pharmaceuticals & Health, Tuesday and Wednesday delivered stronger YoY growth than the traditional peak days. This suggests that instead of waiting for Black Friday or Cyber Monday, shoppers acted as soon as they encountered an offer that met expectations.

This shift aligns with broader retail trends: promotions start earlier each year, shoppers have greater visibility into deals, and loyalty-driven journeys can trigger purchases before the weekend even arrives. Early-week engagement is no longer a side effect, but a meaningful performance driver.

For retailers, this highlights the importance of early campaign activation, value communication, and consistent visibility across the week.

Timing insights

|

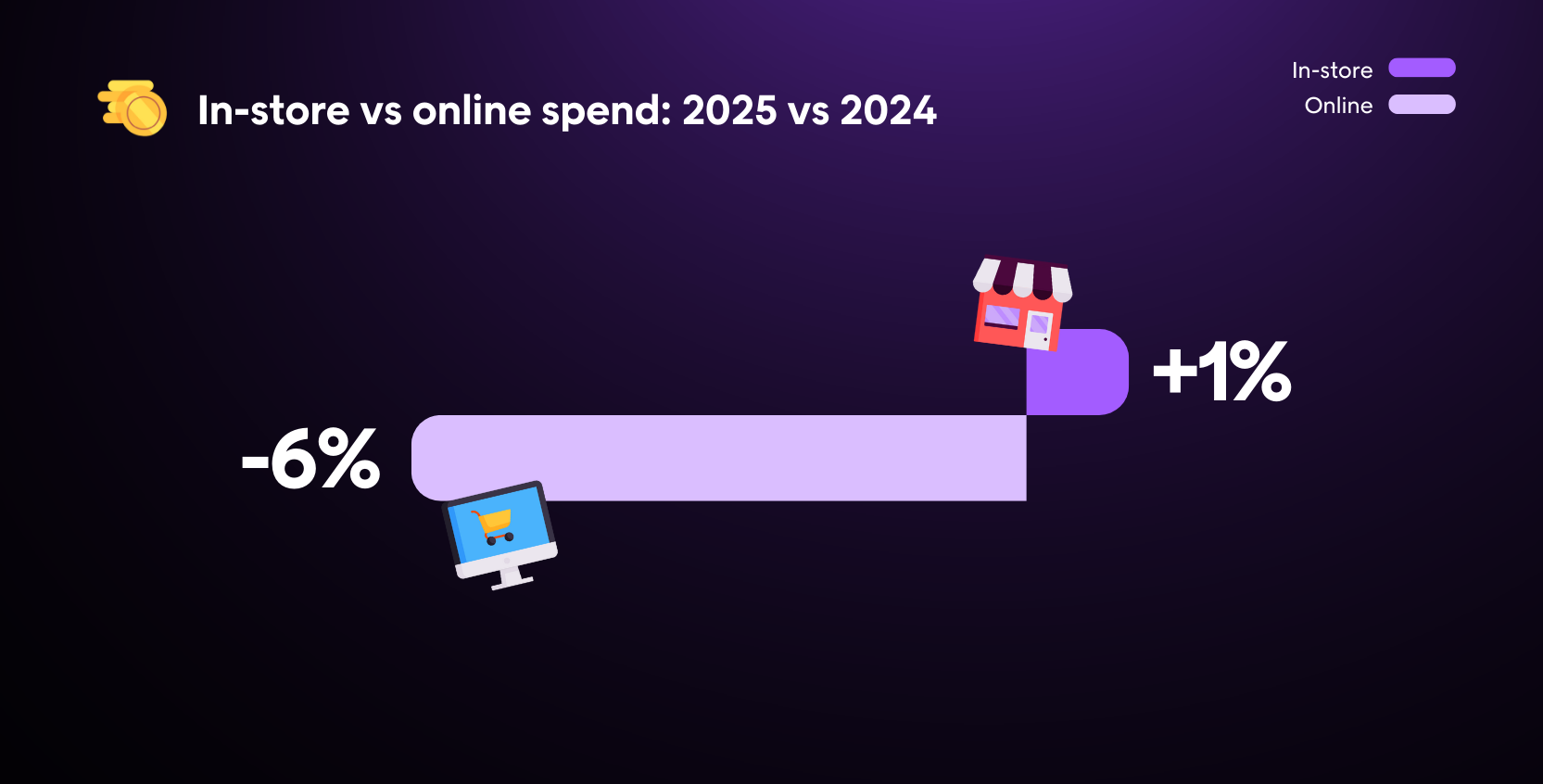

Where shoppers chose to buy: a subtle turn toward stores

Channel performance added another layer to the story. Across all industries, in-store spend increased 1%, while online spend decreased 6%. Although the movement was small, it was consistent and notable across several verticals.

Fashion – Brand led in-store growth with a 12% increase, and Fashion – Premium Brand recorded a 17% rise. Home Decoration & Garden Supplies also saw in-store gains of 6%, and Pharmaceuticals & Health climbed 8% in physical retail.

These results might suggest that tactile experience, immediacy, service, and confidence-building touchpoints continue to play an important role in certain product categories. Meanwhile, online performance varied widely by sector, reinforcing the need for retailers to differentiate digital experiences rather than relying solely on convenience.

Omnichannel behavior is more fluid than ever. Shoppers browse online, compare across channels, and complete their purchases wherever the combination of price, experience, and certainty feels best.

Sector performance reflects broader consumer priorities

Full-week performance across the 11 verticals suggests priorities might be shifting.

Growth in Pharmaceuticals & Health suggests continued investment in wellbeing and essentials. Hobbies & DIY shows that hands-on, at-home creativity remains influential. And Fashion – Brand’s increase could reflect steady interest in quality apparel and lifestyle upgrades.

On the other hand, high-ticket categories faced greater pressure. Furniture, in particular, saw a significant decline, reflecting price sensitivity and cautious decision-making. Beauty & Cosmetics also softened, especially toward the end of the week, suggesting more selective purchasing behavior.

These patterns highlight that Black Week performance is becoming increasingly category-specific, not driven by a single universal trend but by each sector’s unique dynamics and shoppers’ expectations.

Black Friday remains central, but the week is becoming more evenly paced

Black Friday continues to be a significant commercial moment, particularly for sectors where planned purchases and upgrades are a major driver. The results this year suggest that while Black Friday is still highly relevant, shoppers are increasingly comfortable spreading their purchases across more days of the week.

Rather than signaling a shift away from the “big day,” the data points to a more balanced rhythm across the entire week. Black Week is functioning less as a build-up to two peak days and more as a continuous period where different sectors find their own moments of strength. For retailers, this reinforces the value of maintaining visibility and relevance throughout the whole week, not only around the traditional anchor days.

Behind the scenes: How the Voyado platform supported Black Week 2025

Black Week isn’t only a demand peak – it’s also a technical one. From November 24 to December 1, including Cyber Monday, the Voyado platform supported record activity across brands and markets.

Platform performance during the week

|

Behind these numbers is a coordinated, cross-functional effort spanning engineering, operations, product, support, and customer teams.

Erica Sandelin Ekelund, CEO at Voyado, summarized the stakes clearly:

“Black Week is a period where technical performance can directly influence a retailer’s full-year outcome. Ensuring reliability is not just a technical challenge; it is a business-critical responsibility. This year, the suite delivered consistently and at scale, even as volumes reached new highs.”

Looking ahead: what Black Week 2025 means for 2026 strategies

Black Week 2025 reinforced that shopper behavior is evolving. For 2026, retailers can expect continued demand – but also higher expectations for relevance, timing, and experience.

Several themes stand out for next year’s planning:

- Early visibility is essential. Campaigns that resonate early help capture momentum before the weekend.

- Physical stores remain crucial. Customers still value service, fit, reassurance, and immediacy.

- Omnichannel readiness is non-negotiable. Fluid channel-switching means experiences must be cohesive.

- Category-specific strategies drive success. Shoppers behave differently depending on product type, value perception, and context.

Black Week remains a defining moment in the retail calendar – just not in the same way it once was. Retailers who adapt to changing timing, channel behavior, and sector dynamics will be best positioned for success in 2026.

About Author